YPost=β0+β1Group+β2Base+β3Age+β4Z+β5R1+β6R2+ϵ

Stan: Bayesian Modeling Examples

statistics

Sample scripts and examples for Bayesian modeling using Stan.

Keywords

Stan, Bayesian statistics, statistical modeling, MCMC, probabilistic programming, sensitivity analysis, uncertainty analysis, robust analysis

Please don’t mind this post. I use this to try out various highlighting styles for my code and formats.

| {.algorithm} Algorithm 1 Bootstrap Confidence Interval |

| Input: Data X = \{x_1, x_2, ..., x_n\}, statistic \theta(X), confidence level \alpha |

| Output: Confidence interval [\theta_L, \theta_U] |

| 1. for b = 1 to B do - Draw bootstrap sample X_b^* by sampling n observations from X with replacement - Calculate \theta_b^* = \theta(X_b^*) 2. end for 3. Sort \{\theta_1^*, \theta_2^*, ..., \theta_B^*\} in ascending order 4. Set \theta_L = \text{quantile}(\theta^*, \alpha/2) 5. Set \theta_U = \text{quantile}(\theta^*, 1-\alpha/2) 6. return [\theta_L, \theta_U] ``` |

\begin{algorithm}

\caption{Quicksort}

\begin{algorithmic}

\PROCEDURE{Quicksort}{$A, p, r$}

\IF{$p < r$}

\STATE $q = $ \CALL{Partition}{$A, p, r$}

\STATE \CALL{Quicksort}{$A, p, q - 1$}

\STATE \CALL{Quicksort}{$A, q + 1, r$}

\ENDIF

\ENDPROCEDURE

\PROCEDURE{Partition}{$A, p, r$}

\STATE $x = A[r]$

\STATE $i = p - 1$

\FOR{$j = p$ \TO $r - 1$}

\IF{$A[j] < x$}

\STATE $i = i + 1$

\STATE exchange $A[i]$ with $A[j]$

\ENDIF

\ENDFOR

\STATE exchange $A[i + 1]$ with $A[r]$

\RETURN $i + 1$

\ENDPROCEDURE

\end{algorithmic}

\end{algorithm}{js, echo = FALSE}

window.addEventListener('load', (event) => {

elem = document.querySelectorAll("algorithm")

elem.forEach(e => {

pseudocode.renderElement(e, {

indentSize: '1.3em',

commentDelimiter: '//',

lineNumber: true,

lineNumberPunc: ':',

noEnd: false,

captionCount: undefined});

})

});

window.addEventListener('load', (event) => {

elem = document.querySelectorAll(".algorithm")

elem.forEach(e => {

pseudocode.renderElement(e, {

indentSize: '1.3em',

commentDelimiter: '//',

lineNumber: true,

lineNumberPunc: ':',

noEnd: false,

captionCount: undefined});

})

});Y^{\operatorname{Post}} = \beta_{0} + \beta_{1}^{\operatorname{Group}} + \beta_{2}^{\operatorname{Base}} + \beta_{3}^{\operatorname{Age}} + \beta_{4}^{\operatorname{Z}} + \beta_{5}^{\operatorname{R1}} + \beta_{6}^{\operatorname{R2}} + \epsilon

R Markdown

This is an R Markdown document. Markdown is a simple formatting syntax for authoring HTML, PDF, and MS Word documents. For more details on using R Markdown see http://rmarkdown.rstudio.com.

When you click the Knit button a document will be generated that includes both content as well as the output of any embedded R code chunks within the document. You can embed an R code chunk like this:

Stan

data {

int<lower=0> J; // number of schools

real y[J]; // estimated treatment effects

real<lower=0> sigma[J]; // standard error of effect estimates

}

parameters {

real mu; // population treatment effect

real<lower=0> tau; // standard deviation in treatment effects

vector[J] eta; // unscaled deviation from mu by school

}

transformed parameters {

vector[J] theta = mu + tau * eta; // school treatment effects

}

model {

target += normal_lpdf(eta | 0, 1); // prior log-density

target += normal_lpdf(y | theta, sigma); // log-likelihood

}df1 <- read.csv("../../../ts.csv")

df1$y <- ts(df1$Sales)

df1$ds <- as.Date(df1$Time.Increment)

splits <- initial_time_split(df1, prop = 0.5)

train <- training(splits)

test <- testing(splits)

interactive <- TRUE

# Forecasting with auto.arima

library("forecast")

md <- auto.arima(train$y)

fc <- forecast(md, h = 12)

model_fit_arima_no_boost <- arima_reg() %>%

set_engine(engine = "auto_arima") %>%

fit(y ~ ds, data = training(splits))

# Model 2: arima_boost ----

model_fit_arima_boosted <- arima_boost(

min_n = 2,

learn_rate = 0.015

) %>%

set_engine(engine = "auto_arima_xgboost") %>%

fit(y ~ ds + as.numeric(ds) + factor(month(ds, label = TRUE),

ordered = F

),

data = training(splits)

)

# Model 3: ets ----

model_fit_ets <- exp_smoothing() %>%

set_engine(engine = "ets") %>%

fit(y ~ ds, data = training(splits))

model_fit_lm <- linear_reg() %>%

set_engine("lm") %>%

fit(y ~ as.numeric(ds) + factor(month(ds, label = TRUE),

ordered = FALSE

),

data = training(splits)

)

# Model 4: prophet ----

model_fit_prophet <- prophet_reg() %>%

set_engine(engine = "prophet") %>%

fit(y ~ ds, data = training(splits))

# Model 6: earth ----

model_spec_mars <- mars(mode = "regression") %>%

set_engine("earth")

recipe_spec <- recipe(y ~ ds, data = training(splits)) %>%

step_date(ds, features = "month", ordinal = FALSE) %>%

step_mutate(date_num = as.numeric(ds)) %>%

step_normalize(date_num) %>%

step_rm(ds)

wflw_fit_mars <- workflow() %>%

add_recipe(recipe_spec) %>%

add_model(model_spec_mars) %>%

fit(training(splits))

models_tbl <- modeltime_table(

model_fit_arima_no_boost,

model_fit_arima_boosted,

model_fit_ets,

model_fit_prophet,

model_fit_lm,

wflw_fit_mars

)

calibration_tbl <- models_tbl %>%

modeltime_calibrate(new_data = testing(splits))

calibration_tbl %>%

modeltime_forecast(

new_data = testing(splits),

actual_data = df1

) %>%

plot_modeltime_forecast(

.legend_max_width = 25, # For mobile screens

.interactive = interactive

)calibration_tbl %>%

modeltime_accuracy() %>%

table_modeltime_accuracy(

.interactive = FALSE

)| Accuracy Table | ||||||||

| .model_id | .model_desc | .type | mae | mape | mase | smape | rmse | rsq |

|---|---|---|---|---|---|---|---|---|

| 1 | ARIMA(0,1,0) | Test | 3200 | 14.0 | 0.74 | 13.6 | 4252 | NA |

| 2 | ARIMA(0,1,0) W/ XGBOOST ERRORS | NA | NA | NA | NA | NA | NA | NA |

| 3 | ETS(A,N,N) | Test | 3200 | 14.0 | 0.74 | 13.6 | 4252 | NA |

| 4 | PROPHET | Test | 20688 | 96.2 | 4.77 | 62.4 | 22234 | 0.03 |

| 5 | LM | NA | NA | NA | NA | NA | NA | NA |

| 6 | EARTH | Test | 3074 | 12.7 | 0.71 | 12.8 | 4743 | 0.01 |

refit_tbl <- calibration_tbl %>%

modeltime_refit(data = df1)

#> Error:

#> ! object 'calibration_tbl' not found

refit_tbl %>%

modeltime_forecast(h = "4 years", actual_data = df1) %>%

plot_modeltime_forecast(

.legend_max_width = 10, # For mobile screens

.interactive = TRUE

)

#> Error:

#> ! object 'refit_tbl' not foundplot(greybox::forecast(smooth::adam(df1$y, h = 12, holdout = TRUE)))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(greybox::forecast(smooth::es(df1$y, h = 12, holdout = TRUE,

silent = FALSE)))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

s1 <- bayesforecast::stan_naive(ts = df1$y, chains = 4, iter = 4000,

cores = 8)

#> Error:

#> ! object 'df1' not found

plot(s1) + theme_bw()

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 's1' not found

check_residuals(s1) + theme_light()

#> Error:

#> ! object 's1' not found

autoplot(object = forecast(s1, h = 12, biasadj = TRUE, PI = TRUE),

include = 100) + theme_bw()

#> Error:

#> ! object 's1' not found

autoplot(object = forecast(s1, h = 52, biasadj = TRUE, PI = TRUE),

include = 100) + theme_bw()

#> Error:

#> ! object 's1' not found

ztable(summary(s1))

#> Error in `h()`:

#> ! error in evaluating the argument 'object' in selecting a method for function 'summary': object 's1' not found

(meanf(df1$y))

#> Error:

#> ! object 'df1' not found

(forecast(s1, h = 12))

#> Error:

#> ! object 's1' not found

autoplot(object = forecast(s1, h = 6, biasadj = TRUE, PI = TRUE),

include = 100) + theme_bw()

#> Error:

#> ! object 's1' not found

df <- as.data.frame(df1)

#> Error:

#> ! object 'df1' not found

m <- prophet(df1, growth = "linear", yearly.seasonality = "auto")

#> Error:

#> ! object 'df1' not found

future <- make_future_dataframe(m, periods = 60, freq = "months",

include_history = TRUE)

#> Error:

#> ! object 'm' not found

forecast <- predict(m, future)

#> Error:

#> ! object 'm' not found

plot(m, forecast) + theme_bw()

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'm' not found

plot(greybox::forecast(smooth::auto.adam(df1$y, h = 12, holdout = TRUE,

ic = "AICc", regressors = "select")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

adamAutoARIMAAir <- auto.adam(df1$y, h = 50)

#> Error:

#> ! object 'df1' not found

plot(greybox::forecast(adam(df1$y, main = "Parametric prediction interval",

h = 5, sim = 1000, lev = 0.99, interval = "prediction")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(greybox::forecast(auto.adam(df1$y, h = 5, interval = "complete",

nsim = 100, main = "Complete prediction interval")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(greybox::forecast(adam(df1$y, c("CCN", "ANN", "AAN", "AAdN"),

h = 10, holdout = TRUE, ic = "AICc")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(greybox::forecast(adam(df1$y, model = "NNN", lags = 7, orders = c(0,

1, 1), constant = TRUE, h = 5, interval = "complete", nsim = 100)))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(greybox::forecast((adam(df1$y, model = "NNN", lags = c(24,

24 * 7, 24 * 365), orders = list(ar = c(3, 2, 2, 2), i = c(2,

1, 1, 1), ma = c(3, 2, 2, 2), select = TRUE), initial = "backcasting"))))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

adamARIMA

#> Error:

#> ! object 'adamARIMA' not found

# Apply models

adamPoolBJ <- vector("list", 3)

adamPoolBJ[[1]] <- adam(df1$y, "ZZN", h = 10, holdout = TRUE,

ic = "BICc")

#> Error:

#> ! object 'df1' not found

adamPoolBJ[[2]] <- adam(df1$y, "NNN", orders = list(ar = 3, i = 2,

ma = 3, select = TRUE), h = 10, holdout = TRUE, ic = "BICc")

#> Error:

#> ! object 'df1' not found

adamPoolBJ[[3]] <- adam(df1$y, "MMN", h = 10, holdout = TRUE,

ic = "BICc", regressors = "select")

#> Error:

#> ! object 'df1' not found

# Extract BICc values

adamsICs <- sapply(adamPoolBJ, BICc)

#> Error in `UseMethod()`:

#> ! no applicable method for 'logLik' applied to an object of class "NULL"

# Calculate weights

adamsICWeights <- adamsICs - min(adamsICs)

#> Error:

#> ! object 'adamsICs' not found

adamsICWeights[] <- exp(-0.5 * adamsICWeights)/sum(exp(-0.5 *

adamsICWeights))

#> Error:

#> ! object 'adamsICWeights' not found

names(adamsICWeights) <- c("ETS", "ARIMA", "ETSX")

#> Error:

#> ! object 'adamsICWeights' not found

round(adamsICWeights, 3)

#> Error:

#> ! object 'adamsICWeights' not found

adamPoolBJForecasts <- vector("list", 3)

# Produce forecasts from the three models

for (i in 1:3) {

adamPoolBJForecasts[[i]] <- forecast(adamPoolBJ[[i]], h = 10,

interval = "pred")

}

#> Error in `forecast.NULL()`:

#> ! argument "new_data" is missing, with no default

# Produce combined conditional means and prediction

# intervals

finalForecast <- cbind(sapply(adamPoolBJForecasts, "[[", "mean") %*%

adamsICWeights, sapply(adamPoolBJForecasts, "[[", "lower") %*%

adamsICWeights, sapply(adamPoolBJForecasts, "[[", "upper") %*%

adamsICWeights)

#> Error:

#> ! object 'adamsICWeights' not found

# Give the appropriate names

colnames(finalForecast) <- c("Mean", "Lower bound (2.5%)", "Upper bound (97.5%)")

#> Error:

#> ! object 'finalForecast' not found

# Transform the table in the ts format (for convenience)

finalForecast <- ts(finalForecast, start = start(adamPoolBJForecasts[[i]]$mean))

#> Error:

#> ! object 'finalForecast' not found

finalForecast

#> Error:

#> ! object 'finalForecast' not found

graphmaker(df1$y, finalForecast[, 1], lower = finalForecast[,

2], upper = finalForecast[, 3], level = 0.95)

#> Error:

#> ! object 'finalForecast' not found

plot(forecast(forecastHybrid::hybridModel(df1$y, models = "aen",

weights = "equal", cvHorizon = 8, num.cores = 4), h = 5))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

plot(forecast(forecastHybrid::hybridModel(df1$y, models = "fnst",

weights = "equal", errorMethod = "RMSE")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'df1' not found

oesModel <- oes(df1$y, model = "YYY", occurrence = "auto")

#> Error:

#> ! object 'df1' not found

y0 <- stan_sarima(df1$y, refresh = 0, verbose = FALSE, open_progress = FALSE)

#> Error:

#> ! object 'df1' not found

autoplot(forecast(y0, 5, 0.99), "red") + ggplot2::theme_bw()

#> Error:

#> ! object 'y0' not found

df1$month <- lubridate::month(df1$ds)

#> Error:

#> ! object 'df1' not found

gam1 <- mgcv::gam(Sales ~ s(month, bs = "cr", k = 12), data = df1,

family = gaussian, correlation = SARIMA(form = ~month, p = 1),

method = "REML") |>

mgcv::plot.gam(lwd = 3, lty = 1, col = "#d46c5b")

#> Error:

#> ! object 'df1' not foundts_plot(df1, title = "US Monthly Natural Gas Consumption", Ytitle = "Billion Cubic Feet")

#> Error:

#> ! object 'df1' not foundmonths <- c("2022-01-01", "2022-03-01", "2022-06-01")

ubereats <- c(7327.55, 4653.53, 4833.21)

doordash <- c(1304.54, 2000.35, 1643.58)

grubhub <- c(1199.85, 941.68, 623.27)

total <- c(7222.85, 7464.68, 7100.06)

df <- data.frame(months, ubereats, doordash, grubhub, total)

df$months <- as.Date(df$months)

ts_plot(df, title = "US Monthly Natural Gas Consumption", Ytitle = "Billion Cubic Feet")df$total <- ts(df$total)

plot(greybox::forecast(adam(df$total, h = 5, holdout = TRUE,

ic = "AICc", regressors = "select")))

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': The number of in-sample observations is not positive. Cannot do anything.

m <- prophet(df, growth = "linear", yearly.seasonality = "auto")

#> Error in `fit.prophet()`:

#> ! Dataframe must have columns 'ds' and 'y' with the dates and values respectively.

future <- make_future_dataframe(m, periods = 60, freq = "months",

include_history = TRUE)

#> Error:

#> ! object 'm' not found

forecast <- predict(m, future)

#> Error:

#> ! object 'm' not found

plot(m, forecast) + theme_bw()

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'm' not found# Plotting actual vs. fitted and forecasted

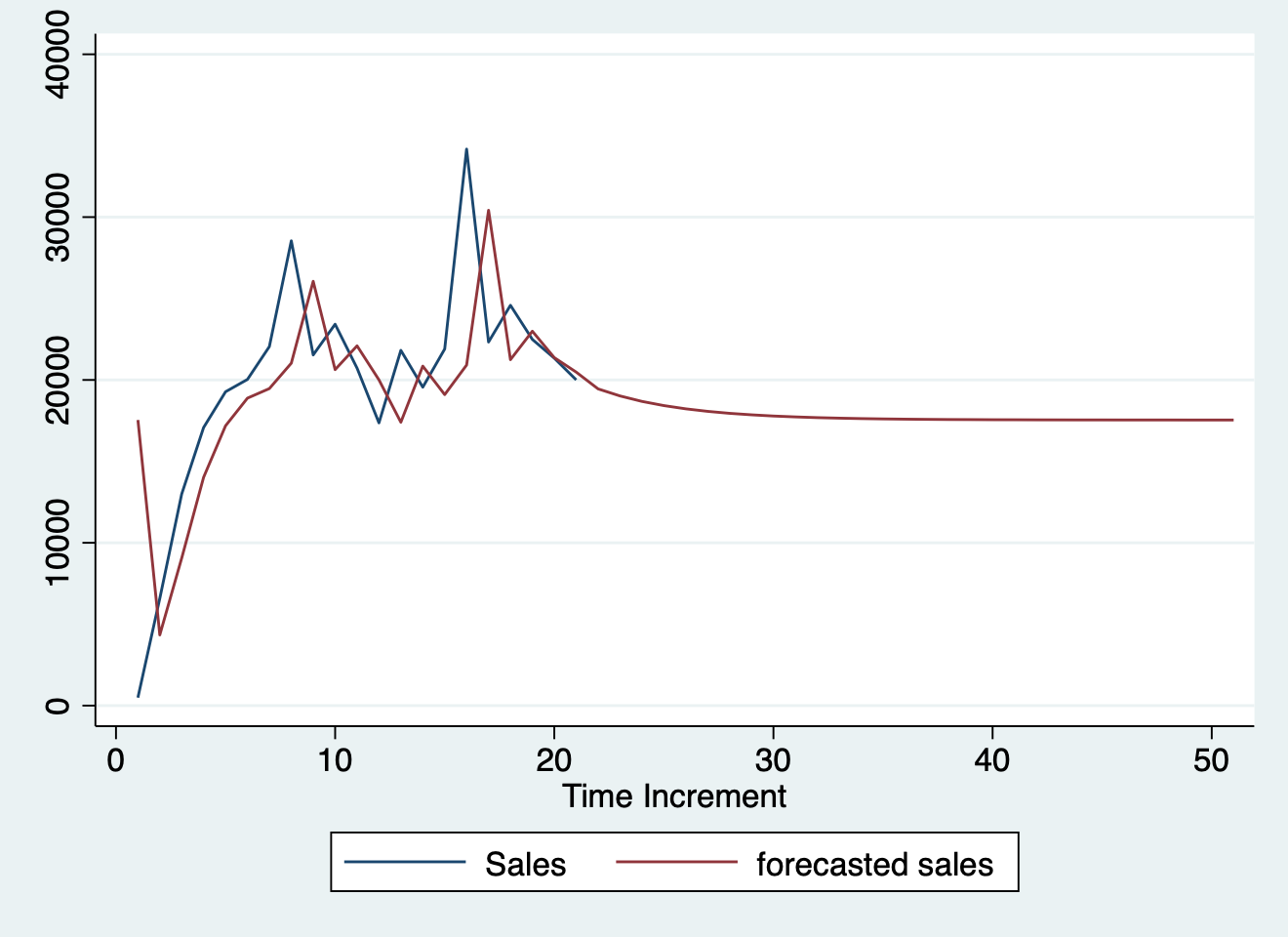

test_forecast(actual = df1$y, forecast.obj = fc, test = test$y)

#> Error:

#> ! object 'fc' not found

plot(fc)

#> Error in `h()`:

#> ! error in evaluating the argument 'x' in selecting a method for function 'plot': object 'fc' not foundimport delimited "../../../ts.csv", clear

#> (encoding automatically selected: ISO-8859-1)

#> (5 vars, 21 obs)

#>

#>

#> -initialize- invalid parallel subcommand (help parallel)

#> r(198);

#>

#> r(198);

Python

from pandas import DataFrame

#> ModuleNotFoundError: No module named 'pandas'

import statsmodels.api as sm

#> ModuleNotFoundError: No module named 'statsmodels'

import matplotlib as plot

#> ModuleNotFoundError: No module named 'matplotlib'

Stock_Market = {'Year': [2017,2017,2017,2017,2017,

2017,2017,2017,2017,2017,

2017,2017,2016,2016,2016,

2016,2016,2016,2016,2016,

2016,2016,2016,2016],

'Month': [12, 11,10,9,8,7,6,5,4,

3,2,1,12,11,10,9,8,7,6,

5,4,3,2,1],

'Interest_Rate':[2.75,2.5,2.5,2.5,2.5,2.5,

2.5,2.25,2.25,2.25,2,2,2,1.75,1.75,

1.75,1.75,1.75,1.75,1.75,1.75,1.75,1.75,1.75],

'Unemployment_Rate':[5.3,5.3,5.3,5.3,5.4,5.6,

5.5,5.5,5.5,5.6,5.7,5.9,6,5.9,5.8,6.1,

6.2,6.1,6.1,6.1,5.9,6.2,6.2,6.1],

'Stock_Index_Price': [1464,1394,1357,1293,1256,1254,1234,1195,1159,1167,1130,

1075,1047,965,943,958,971,949,884,866,876,822,704,719]

}

df = DataFrame(Stock_Market,columns=['Year','Month','Interest_Rate',

'Unemployment_Rate','Stock_Index_Price'])

#> NameError: name 'DataFrame' is not defined

X = df[['Interest_Rate','Unemployment_Rate']]

#> NameError: name 'df' is not defined

# here we have 2 variables for the multiple linear regression. If you just want to use one variable for simple linear regression, then use X = df['Interest_Rate'] for example

Y = df['Stock_Index_Price']

#> NameError: name 'df' is not defined

X = sm.add_constant(X) # adding a constant

#> NameError: name 'sm' is not defined

model = sm.OLS(Y, X).fit()

#> NameError: name 'sm' is not defined

predictions = model.predict(X)

#> NameError: name 'model' is not defined

print_model = model.summary()

#> NameError: name 'model' is not defined

print(print_model)

#> NameError: name 'print_model' is not definedR

fit <- glm(mpg ~ cyl + disp, mtcars, family = gaussian())

# show the theoretical model

equatiomatic::extract_eq(fit)E( \operatorname{mpg} ) = \alpha + \beta_{1}(\operatorname{cyl}) + \beta_{2}(\operatorname{disp})

Stata

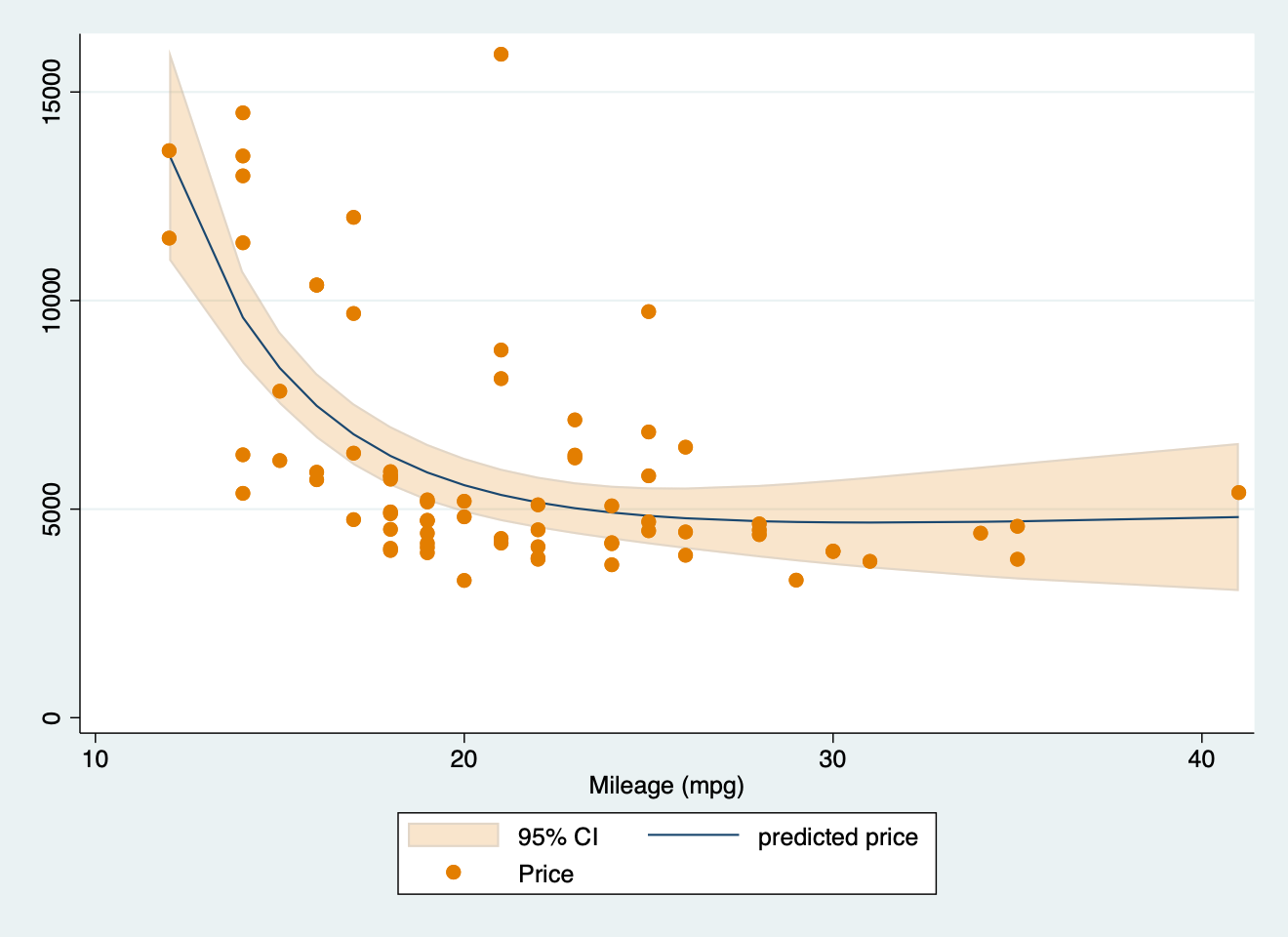

sysuse auto2, clear

parallel initialize 8, f

mfp: glm price mpg

twoway (fpfitci price mpg, estcmd(glm) fcolor(dkorange%20) alcolor(%40)) || scatter price mpg, mcolor(dkorange) scale(0.75)

graph export "mfp.png", replace

#> . sysuse auto2, clear

#> (1978 automobile data)

#>

#> . parallel initialize 8, f

#> -initialize- invalid parallel subcommand (help parallel)

#> r(198);

#>

#> r(198);

clear

set obs 100

/**

Generate variables from a normal distribution like before

*/

generate x = rnormal(0, 1)

generate y = rnormal(0, 1)

/**

We set up our model here

*/

parallel initialize 8, f

bayesmh y x, likelihood(normal({var})) prior({var}, normal(0, 10)) ///

prior({y:}, normal(0, 10)) rseed(1031) saving(coutput_pred, replace) mcmcsize(1000)

/**

We use the bayespredict command to make predictions from the model

*/

bayespredict (mean:@mean({_resid})) (var:@variance({_resid})), ///

rseed(1031) saving(coutput_pred, replace)

/**

Then we calculate the posterior predictive P-values

*/

bayesstats ppvalues {mean} using coutput_pred

#> . clear

#>

#> . set obs 100

#> Number of observations (_N) was 0, now 100.

#>

#> . /**

#> > Generate variables from a normal distribution like before

#> > */

#> . generate x = rnormal(0, 1)

#>

#> . generate y = rnormal(0, 1)

#>

#> . /**

#> > We set up our model here

#> >

#> > */

#> . parallel initialize 8, f

#> -initialize- invalid parallel subcommand (help parallel)

#> r(198);

#>

#> r(198);library(lme4)

library(simr)

# Toy model

fm = lmer(y ~ x + (x | g), data = simdata)

# Extend sample size of `g`

fm_extended_g = extend(fm, along = 'g', n = 4)

# 4 levels of g

pwcurve_4g = powerCurve(fm_extended_g, fixed('x'), along = 'g', breaks = 4,

nsim = 50, seed = 123,

# No progress bar

progress = FALSE)

# 6 levels of g

# Create a destination object using any of the power curves above.

all_pwcurve = pwcurve_4g

# Combine results

all_pwcurve$ps = c(pwcurve_4g$ps[1])

# Combine the different numbers of levels.

all_pwcurve$xval = c(pwcurve_4g$nlevels)

print(all_pwcurve)

#> Power for predictor 'x', (95% confidence interval),

#> by number of levels in g:

#> 4: 44.00% (29.99, 58.75) - 40 rows

#>

#> Time elapsed: 0 h 0 m 4 s

plot(all_pwcurve, xlab = 'Levels of g')

https://www.datacamp.com/datalab/w/2c40d510-1d81-4078-8ae3-9dcdd8f2a21b/edit#welcome-environment

https://www.datacamp.com/datalab/w/bf3f12b6-9b15-400f-8f0e-674b33b29cbe/print-report/notebook.ipynb#1-load-your-datahttps://www.datacamp.com/datalab/w/2c40d510-1d81-4078-8ae3-9dcdd8f2a21b/edit#considered-exemption

Citation

BibTeX citation:

@misc{panda2018,

author = {Panda, Sir},

title = {Stan: {Bayesian} {Modeling} {Examples}},

date = {2018-01-01},

url = {https://lesslikely.com/posts/statistics/stan},

langid = {en},

abstract = {Sample scripts and examples for Bayesian modeling using

Stan.}

}

For attribution, please cite this work as:

1. Panda S. (2018). ‘Stan: Bayesian Modeling Examples’.

Less Likely. https://lesslikely.com/posts/statistics/stan.